Turning Markowitz Portfolios Into Index Trackers

Practical Guide to Benchmark-Aware Portfolio Optimization

One of the neat surprises in portfolio theory is that you can take a regular Markowitz portfolio and turn it into an index-tracking portfolio with nothing more than a single correction term. Instead of rebuilding the whole optimization, you just nudge the MV weights in a very specific direction. In the paper I’m summarizing here, the author shows exactly how this works: add a constant adjustment vector, and suddenly the portfolio lines up much more closely with the benchmark. What is even more interesting is that this “tracking-efficient” (TE) version consistently performs better for benchmark-following purposes, such as higher beta, slightly more variance, and much lower tracking error compared to the traditional MV portfolio.

Most investors, fund managers measure themselves against a benchmark like the S&P500 (Index Fund), but the classical Markowitz portfolio (Mean-Variance Optimization) fails to track the index because it only minimizes the portfolio variance for a given target, which leads to what we often see in practice —

a. portfolio with extreme long/short weights

b. high tracking error

c. portfolios that drift far from the market

This is where Index-Tracking Optimization comes in.

Index-tracking portfolio = Markowitz portfolio + one simple correction term

Instead of minimizing the historical tracking error, the author defined risk as the variance of tracking error.

since the market variance is constant and doesn’t depend on the portfolio weight, the final objective function and the equality constraints — budget & expected return constraints.

Here,

The goal is to minimize the volatility and increase the alignment with the index.

To solve the objective function, the author set up a Lagrangian with two constraints on return and budget, and took the derivative to obtain the KKT conditions. These conditions form a linear block-matrix system that can be solved in closed form using a projection matrix Q.

This leads to the key result of the paper: the tracking-efficient (TE) portfolio is simply the Markowitz portfolio plus a correction term that improves index alignment:

To summarize the author’s main theoretical insight, the tracking-efficient (TE) portfolio is essentially just the Markowitz (MV) portfolio with a smart adjustment added on top. This adjustment term depends only on the betas, the covariance, and the variance of the benchmark index. Also, it tells us exactly how each weight shifts when we move from MV optimization to TE optimization, and depending on the sign of this shift, the TE portfolio will either increase or decrease exposure to a given asset. Thus, the paper also shows that TE portfolios consistently have higher beta and slightly higher variance than their MV counterparts, but in return, they achieve strictly lower tracking-error variance.

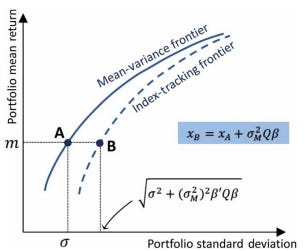

In the figure below, we see that the index-tracking portfolio sits relative to the traditional Markowitz efficient frontier. Point A represents the MV-optimal portfolio for a chosen return level m. But when we shift to the tracking-efficient framework, the portfolio moves to point B, which lies on a separate “index-tracking frontier.” The return stays the same, but the risk (standard deviation) increases slightly by a predictable amount. This shift happens because the TE portfolio adjusts weights to better follow the benchmark, which naturally raises beta and variance while reducing tracking error.

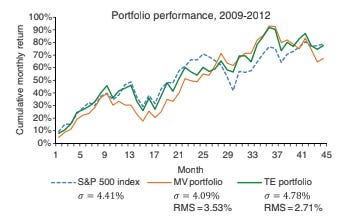

To illustrate the theory author uses five large technology stocks (AAPL, CSCO, IBM, MSFT, ORCL) to show how an MV portfolio differs from a tracking efficient (TE) portfolio, where the goal is to follow the S&P500, using data from 2009-2012. The results show the MV portfolio taking extreme positions (IBM at 97.5%) and multiple shorts. But the TE drove a far more balanced portfolio with IBM weights dropping to 53% and only one stock remaining slightly short.

In conclusion, we can see in the above figure that the TE portfolios are much closer to the S&P500 than the MV portfolios with only 5 stocks.